If you’ve just been in a car accident, your mind is likely racing in two completely different directions. Looking out at the road, you see your crumpled car and wonder, “How am I going to get to work tomorrow? Who is paying for the tow truck?” But the moment the adrenaline wears off, a much heavier panic sets in: the throb in your neck, the shooting pain in your back, and the terrifying realization that medical bills are about to start piling up while you’re missing work.

Table of Contents

Dealing with an insurance company during this time can feel like trying to speak a foreign language while underwater. Adjusters often treat you like a claim number, dragging their feet on your car repairs while secretly hoping you’ll settle your medical claim for pennies before you even know the true extent of your injuries. It is incredibly stressful, but you do not have to figure it out blindly.

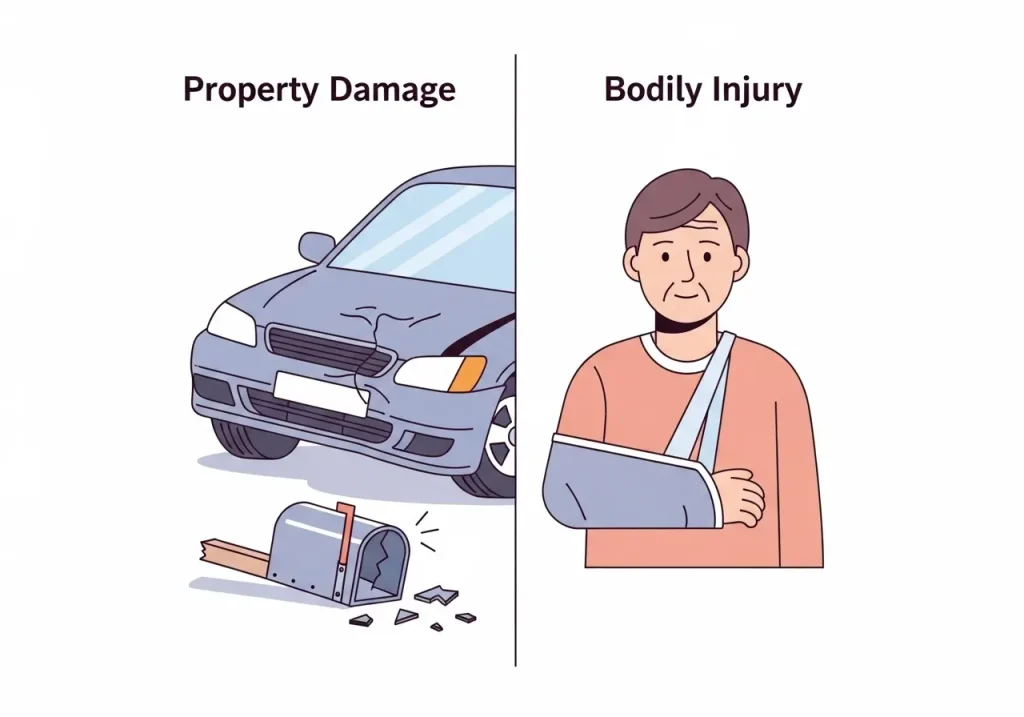

When you file an insurance claim after an accident, you are actually dealing with two entirely separate claims under the law: Property Damage (PD) and Bodily Injury (BI). Understanding how these two paths move at completely different speeds is the absolute key to protecting your physical recovery and your wallet.

Property Damage vs. Bodily Injury: The Critical Differences

The biggest trap accident victims fall into is treating their accident as a single, massive insurance claim. Competitor sites, like standard corporate law firm blogs, often give vague, academic definitions of these terms without explaining how they actually interact in the real world.

In simple terms, Property Damage covers stuff, while Bodily Injury covers people. Because a vehicle’s value is easy to calculate, your property damage claim can often be resolved in a matter of weeks. Your bodily injury claim, however, must take much longer because the true cost of human healing cannot be calculated overnight.

| Feature | Property Damage (PD) Claim | Bodily Injury (BI) Claim |

| What It Covers | Vehicle repairs, total loss payouts, rental cars, personal items inside the car (e.g., car seats, laptops). | Emergency room visits, surgeries, physical therapy, lost wages, future medical care, and pain and suffering. |

| Resolution Timeline | Fast (usually 2 to 6 weeks). | Slow (months to over a year; depends heavily on medical healing). |

| When to Settle | As soon as you agree on a fair repair estimate or fair market value for a totaled vehicle. | Only after you reach Maximum Medical Improvement (MMI). |

| Impact of Fault | Depends on state negligence laws, but property values are fixed numbers. | Heavily impacted by state liability rules, which can slash your payout if you share fault. |

State-Specific Nuances: How Location Changes Your Payout

1. No-Fault vs. At-Fault States

In “No-Fault” states like Pennsylvania (PA), your own insurance policy’s Personal Injury Protection (PIP) pays for your medical bills up to a certain limit, regardless of who caused the crash. However, your Property Damage claim is still filed against the at-fault driver’s insurance. In purely “At-Fault” states like Arizona (AZ) or Missouri (MO), the negligent driver’s insurance is on the hook for both your medical bills and your car repairs from day one.

2. Comparative Negligence Rules

If an adjuster can prove you were even slightly responsible for the crash, your state’s laws dictate how much money is chopped from your settlement:

Pure Comparative Fault (e.g., Arizona, Missouri): You can recover compensation even if you were 99% at fault, but your payout is reduced by your percentage of blame. If your bodily injury claim is worth $100,000 but you are found 20% at fault, you receive $80,000.

Modified Comparative Fault (e.g., Pennsylvania, Connecticut): You can only recover money if your fault is 50% or less (or 51% depending on the state). If you cross that line, you get zero for both bodily injury and property damage.

The State Chart Trap: Be careful when looking at generic online settlement charts. An injury that pays out highly in a state with voter-friendly insurance laws might be severely restricted in another due to local tort thresholds. To see exactly how your state’s laws apply to your unique accident data, use our free Personal Injury Settlement Calculator. It requires no registration and instantly adapts to your specific jurisdiction.

The Valuation Breakdown: What is Your Claim Actually Worth?

When calculating a Bodily Injury settlement, the law splits your compensation into two distinct buckets: Economic Damages and Non-Economic Damages.

Economic Damages (The Paper Trail)

These are your objective, measurable financial losses. They are proven using receipts, bills, and pay stubs.

Past and Future Medical Expense: Every ambulance ride, ER visit, X-ray, and future physical therapy session.

Lost Wages and Lost Earning Capacity: The time you missed at work immediately following the crash, plus any long-term reduction in your ability to earn a living.

Non-Economic Damages (The Human Cost)

This is what the insurance industry calls Pain and Suffering. It compensates you for physical agony, mental anguish, loss of enjoyment of life, and the emotional trauma of the wreck.

Realistic Settlement Benchmarks

Insurance adjusters use a “multiplier method” to calculate pain and suffering, multiplying your economic damages by a number between 1.5 and 5 depending on severity.

Minor Injuries ($5,000 – $25,000): Soft tissue injuries like whiplash, minor strains, or bruising. Property damage is usually light to moderate. Payouts cover brief medical treatment and a small amount for a few weeks of discomfort.

Moderate Injuries ($25,000 – $100,000): Fractures, torn ligaments, or concussions requiring ongoing physical therapy or minor specialist procedures. Property damage is often severe or a total loss.

Severe/Severe Permanent Injuries ($100,000+): Spinal cord damage, traumatic brain injuries (TBI), or surgeries with permanent hardware placement. These claims require calculating massive future medical care costs.

4 "Insider" Traps That Can Destroy Your Claim Value

Insurance companies train their adjusters to look for ways to devalue your claim. If you know their playbook, you can easily protect your rights by avoiding these four critical pitfalls:

1. The Insurance “First Offer” Trap

Within days of the accident, an adjuster might call and offer you a quick check say $2,500 to settle your bodily injury claim. They will sound incredibly friendly and empathetic. Do not sign it.

Once you sign a release, your claim is dead forever. If you find out three months from now that you have a herniated disc requiring a $50,000 surgery, you cannot ask for another dime. Never settle your injury claim until you reach Maximum Medical Improvement (MMI) the point where your doctors declare you are either 100% healed or as healed as you are ever going to get.

2. The 72-Hour Medical Window

If you didn’t go to the hospital straight from the accident scene, you must see a doctor within 72 hours. Even if you think it’s just minor soreness, many severe internal injuries or spinal issues are masked by adrenaline for days. If you wait two weeks to see a doctor, the insurance adjuster will write in their files: “If they were truly hurt, they wouldn’t have waited 14 days to seek care. The injury must have happened somewhere else.”

3. The Social Media Blackout

Assume the insurance adjuster is actively monitoring your public Facebook, Instagram, and TikTok profiles. If your bodily injury claim states that you have severe, debilitating back pain, but you post a photo smiling at a friend’s backyard barbecue or a family dinner, the insurance company will use it in court to argue that you are exaggerating your injuries. Go on private mode, and stop posting until your claim is entirely resolved.

4. The Pain Journal

While economic damages are easy to track with medical bills, non-economic damages (pain and suffering) can be hard to prove months down the road. Start a daily log either in a physical notebook or a private notes app. Track your daily physical pain levels on a scale of 1 to 10, document the activities you missed (like being unable to lift your toddler or sleep through the night), and record how your injuries affect your mental well-being. This acts as concrete, unshakeable evidence during settlement negotiations.

Calculate Your True Settlement Potential Right Now

Property damage claims can generally be handled on your own by dealing directly with the body shops and getting your vehicle fixed or replaced. But when it comes to bodily injury, the financial stakes are simply too high to guess at the numbers or accept the insurance adjuster’s lowball calculations.

You shouldn’t have to surrender your personal data or pay a lawyer a heavy fee just to find out what a fair settlement range looks like for an accident like yours.

Before you speak to an insurance adjuster or sign any paperwork, get a clear, data-driven baseline. Use the free, 100% confidential Personal Injury Settlement Calculator. It factors in your specific state laws, your property damage values, and your medical expenses to give you an honest look at what your combined claims are truly worth.

Disclaimer

The information provided in this article is for educational and informational purposes only and does not constitute formal legal or medical advice. Because personal injury and insurance laws vary drastically by state and are subject to change, using this material or the online calculator tool does not create an attorney-client relationship. If you have been injured in an accident, always consult with a licensed professional or qualified attorney in your jurisdiction to discuss the specific details of your case.